Chipotle - Investment Thesis

Not so fast, a not so casual company

Company Overview

Chipotle Mexican Grill, Inc., commonly known as Chipotle, is a prominent player in the fast-casual restaurant industry. Founded in 1993, the company has grown to become a recognized brand globally, offering a menu focused on customizable Mexican-inspired cuisine, which features a relevant menu of burritos, burrito bowls (a burrito without the tortilla), quesadillas, tacos, and salads.

As of June 30, 2023, the company owns and operates (no franchised restaurants like Mcdonald's or Domino’s) 3,268 restaurants including 3,205 Chipotle restaurants within the US, 57 international Chipotle ( Canada, the UK, France, and Germany) restaurants and 6 non-Chipotle restaurants. Operates 26 owned distribution centers and employs more than 100,000 people.

Chipotle is celebrating this year its 30th anniversary since its foundation in 1993 by Steve Ells, a chef and entrepreneur who dreamed of opening a fine dining restaurant. Chipotle was meant to be the cash generator to make this dream true, but the business was too good and that dream was replaced by a TexMex fast-casual restaurant chain. The secret sauce of its business is quality, convenience, and efficient operations.

The trust broke from 2015 to 2018 given a series of foodborne illnesses. Since then, the chain has been adapting rapidly to regain the trust of customers.

The company has carved out an enduring niche in the U.S. restaurant landscape, with competitive menu prices, extreme convenience, and" food with integrity" allowing the firm to lure away customers from both casual dining and traditional fast-food competitors.

Source: company

Source: own elaboration

A bit of History

Chipotle is celebrating this year its 30th anniversary since its foundation in 1993 by Steve Ells, a chef and entrepreneur who dreamed of opening a fine dining restaurant. Chipotle was meant to be the cash generator to make this dream true, but the business was too good and that dream was replaced by a TexMex fast-casual restaurant chain.

He eventually brought the company public in 2006 and served as the CEO until late 2017. Today he serves as the executive chairman of Chipotle and he's kind of known as the grandfather of fast casual dining. He started the restaurant with an $85,000 loan from his father and they figured if they could scrap around enough demand for 100 burritos a day, they could break even, but quickly they were selling well over 1,000 burritos per day. He set up a model that was recognized for an open kitchen using fresh ingredients with real cooking in the back and a defacto assembly line in the front that allowed for customization and speed that's kind of become its own industry standard.

However, this love story was going to have its moment of truth. 2015 was a turning point for Chipotle. In the second half of the year, a food-safety crisis erupted. Around 500 people became ill from E. coli, salmonella, and norovirus after eating at the company’s restaurants. This badly affected consumer confidence at Chipotle, which manifested in the sharp declines in the company’s same-store sales growth and average restaurant sales in 2016. What were initially strengths – Chipotle’s food and people culture – ended up causing problems for the company. These episodes shocked the stock performance with a drawdown higher than 60%.

After the late 2015 food safety issue flared up, Ells and his team embarked on fixing the issues at the company. But they struggled, and 2016 became a painful year for Chipotle. Monty Moran left as Co-CEO in late December 2016; around a year later, Ells stepped down from his CEO position and assumed the role of executive chairman. Ells left Chipotle completely in March this year. Brian Niccol, who already had leadership experience at a fast food chain (Taco Bell), succeeded Ells as CEO in March 2018. Niccol and his team have managed to retain what is special about Chipotle while improving the areas that needed fixing.

The context in which it operates

The US fast-casual restaurant market is estimated to grow at a CAGR of 11.56% between 2022 and 2027. The size of the market is forecast to increase by USD 55.4 billion. The growth of the market depends on several factors, including demand for innovation and customization in food menus, changing lifestyles, and rise in demand for on-the-go food, and a growing demand for gluten-free dining.

At a high level, we can see a healthy growth in restaurant sales, a 5,9% CAGR between 2023 and 2003, higher than inflation. A tailwind to keep in mind in general terms.

Source: Federal Reserve

Based on food type, the Asian/Latin American food segment is predicted to account for a significant market share in the fast-casual restaurant industry. This increase can be attributed to the increased demand for international cuisine among consumers. The demand for innovation and customization in food menus is notably driving the market growth, although factors such as intense competition from quick-service restaurants may impede the market growth.

Source: technavio.com

Mexican is only behind American and Pizza/Italian when it comes to the number of restaurants. Quick-service restaurants account for 8.2% of all Mexican restaurants, while fine dining accounts for just 1.3% of all restaurants in the category. Taco Bell has the largest share of the U.S. Mexican food market, with more than 7,700 locations. Taco Bell accounts for 9.6% of all Mexican restaurants in the U.S. and more than one in four (26.4%) of all Mexican chain restaurants. Chipotle, Qdoba, Moe’s Southwest Grill, and Del Taco round out the top five in terms of most popular U.S. chains. In all, there are more than 80,000 Mexican restaurants in the U.S., accounting for almost 10 percent (9.4%) of total U.S. restaurants.

Source: own elaboration

Although Chipotle is in the second position, according to a 2022 survey by Mashed, 41.83% of people prefer Chipotle to other quick-service Mexican restaurants. The survey by Mashed only took the above five options into account. After Chipotle and Taco Bell (26.24%) the list of best Mexican food chains were Moe's Southwest Grill (13.88%), Qdoba (11.41%), and Del Taco (6.65%). A good sign for growing also gaining more market share.

About 37% of all U.S.-based Mexican restaurants are quick service, making the sector the largest segment of the market. While a bulk of all U.S.-based Mexican restaurants are quick service or fast food, one-quarter (26%) are casual dining. Only 7% of Mexican restaurants in the U.S. are food trucks, 3% are ghost kitchens and only 98 total U.S. Mexican restaurants are considered fine dining.

Another topic to be discussed is the aggregators. Online ordering has been a major source of growth in recent years and where the company is investing heavily, as it should considering that 40% of the sales are digital. In that regard, we could say that Chipotle is a late player, with room to improve, and a lack of culture for this cuisine, or a little of each. Among the top sources for digital ordering in terms of market share, there’s no sign of Chipotle. Considering Mexican food is only behind Italian/pizza options, I consider it more as an opportunity to conquer:

Source: own elaboration and statista.

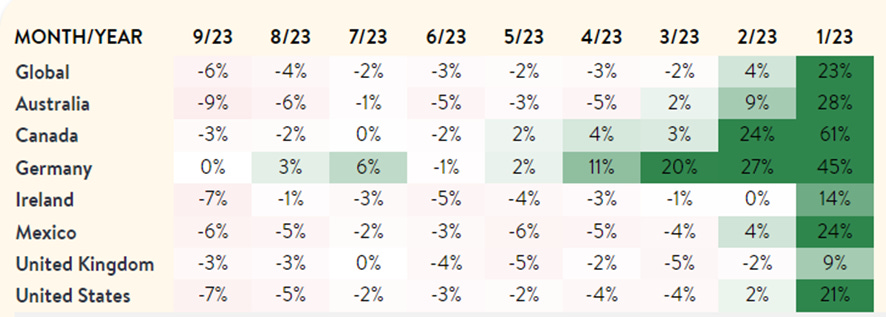

One last thing to consider is real data from restaurant reservations. Sure Chipotle is not one of those restaurants, but it may well be a good and quick reference point to check in consumption tendencies. The volume of seated diners in 2023 vs. 2022 is decreasing, and accelerating. It normally takes a year and a year and a half for a macro reaction to interest rate hikes. In my opinion, it makes sense.

Source: opentable.com

Business Model

We could say that Chipotle is the father of the fast-casual category, its model business rely on this space where customers don’t require a full-service experience but demand a higher quality than fast food chain have to offer. Fresh food in the whole supply chain, is a healthy proposition to choose between 53 ingredients with the rapidness of serving 100 customers in 15 minutes, and with a small premium over fast food chains. A good value proposition from the customer's standpoint and for business.

Source: Own elaboration

Digital transformation is a great part of the current narrative for the business model for Chipotle. It started in 2008 without any relevancy, which would change many years after the pandemic when the digital market share soared from a 17% level to 70%. It has now moderated, although 40% is a pretty high level. This customer behavior change produces changes in the company at its core. For instance, in the restaurants they have two separate prep stations called make lines. One is for just in-store orders, and the other one is for digital and catering orders. Another consequence is the implementation of what is called Chipotlane or digital kitchens. First Chipotle opened in 2018 and now they have more than 600 across the US. Currently, almost 80% of the new locations will have their own Chipotlane.

Source: Own elaboration

Source: company

Another thing to consider of high value is the loyalty membership. Even Chipotle has been one of the later movers in that space, its popularity has increased rapidly and currently, more than 30 million members are subscribed for the benefits they offer in exchange for data mainly and of course, as the name says, loyalty, which means recurrence, recurrent revenues, higher average tickets, and thus, higher multiples. Starbucks's loyal program is a reference as a business practice, and without evaluating the outcome, the number is members is very similar, over 30 million too.

This loyalty program is wisely combined with social media, where they work to generate engagement through viral challenges, a “freepotle” prize wheel event in TikTok Live and Instagram Live. All these elements feed what is known by Chipotle’s Digital Flywheel, to segment, customize, predict, manage better, and be the first mover on new trends.

Digitalization, luckily, does not end here. I brought up previously Chipotlane, normally the cost of a new restaurant is around $1 million. With Chipotlane, the incremental cost is $75-100k, which comes with an incremental $200k in annual revenue. Fostering digital business eliminates a share of the main cost elements, which produces in return a higher return.

In terms of costs, food, beverage and packaging; labor; occupancy, and others are the main categories to consider. It’s good to see how the penetration has an upward trend.

Source: company

As the digitalization is growing, new sources of growth have been unlocked. Digital kitchens only have the capability to serve online orders, and they come with one major benefit, they provide a financial profile fit for smaller locations and they can consider opening this new digital kitchen where the population nearby is higher than 40k residents. This perk unlocks new locations, allowing a higher level of penetration or business scalability capacity.

Caption: the first opened in December 2021

But as we know, 2022-2023 has been a great year in terms of technology progress. Let’s have a look at what we could expect from Chipotle in the near future.

Today, Chipotle has two big ambitions when it comes to technology: AI and robotic meal preparation. They are working with its cloud provider Microsoft, to use their AI capabilities and machine learning services to develop fully automated order-taking and processing. The second is to roll out advanced robotic meal preparation equipment across its restaurants. Last year, Chipotle launched its very own venture capital fund (Cultivate Next) which took a stake in Hyphen, developer of the Makeline Kitchen Robotics equipment, and the two firms have started work on digitally enabled, automated order preparation as we can see in the picture below. Besides, they developed a new, simpler machine, called Autocado to cut, core, and peel avocados used to prep guacamole and they will be tracking inventory in the upcoming months through RFID technology, to work with its suppliers with restaurants' real-time data.

Source: Nation’s restaurant news.

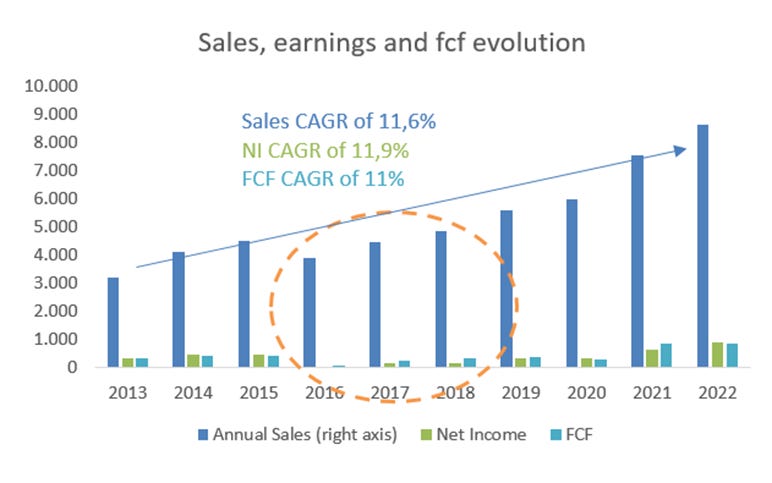

Let’s discuss unit economics. Chipotle, unlike Domino's, does not offer franchise opportunities, they decided to keep the profits even though the unit-level margin is best in class. The company owns and operates the great majority of its restaurants. Revenues first.

Source: company and own elaboration

Revenue levers are pretty decent and trending upwards, being 2022 a new record in sales per store. 2016 was a bad year for the food poisoning concern, although it only took one year to recover growth. I’m taking a big jump, but the next step is margin, a new all-time high published in the second quarter.

Source: company and own elaboration

In the end, what all this means is that if the company requires around a million to start a new normal restaurant and considering a 25% margin on 2,8 million in sales, we’re looking at around $700.000 EBITDA. Less than two years for a full payback, and later on, cash flows to feed the growth machine.

A couple more things that make this business a good business.

· Transparency and in-store experience. Normally, in a McDonald’s ordering experience, you generally order at the counter or in the machine, wait, and leave. Chipotle has the benefit of moving you through the line as they're assembling your order. You are seeing the fresh ingredients of what you are going to eat and how it is prepared. It may take between 30 seconds or a minute, but the feeling is completely different.

· Predictability. Nowadays, they have tons of data to work with, and that allows them a high degree of certainty. They're able to know how much food they need and when. They do a great job at having the food available for their customers when they want it, and it's about the continuity of that throughput.

· Healthy food. Eating healthy is a trend that started years ago, and it’s going to continue and accelerate. Chipotle displays calories, fat, protein, and carbohydrates. That’s absolutely important for someone who cares about their nutrition, and considering the infinite combinations you can do with 53 ingredients, for the price they’re asking you, the value proposal is higher than they consider.

· Workforce. The company treats really well the staff, with a good salary, career opportunities, equity share, performance, and safety incentives. Although the cost is definitely higher for the company, the return on commitment, and low turnover, make it possible for this business where treating fresh ingredients has a long learning curve. In 2022, Chipotle promoted over 22K employees and 90% of restaurant management roles were internal promotions. The company calls it, the Restaurateur program. The program, which started in 2005, is meant to improve employee performance at each restaurant while providing excellent career prospects.

Source of Growth

A company with this type of business model, and with the intention to keep it this way, has three different sources of growth:

1. Growth coming from restaurants already deployed.

2. The opening of new locations.

3. Higher margins.

1. Comp Sales Growth

In an interview, the CEO, Brian Niccol said: “We've talked about getting to three million average unit volumes. The good news is we're closing in on that. We're now starting to set our sights on 3.5, 4 million average unit volumes out of our existing restaurants”.

Source: company and own elaboration

Considering past growth, even with food poisoning news, and projecting it, the company should achieve the $4 million target for 2031. It’s a possible scenario.

2. New locations

Again, the expectations set by its CEO words: “You've seen the number that we're targeting, 7,000 restaurants in the United States and Canada. We'll probably finish this year just shy of 3,500 restaurants, so we're getting halfway there. If you start to do the math on this, you can see a quick path to how you can easily double this business again in a big way, both in restaurant count and revenue. We're really optimistic about that. Then we're just getting started, frankly, with some international expansion. We're in the early days in Western Europe, but we're continuing to see really good top-line growth in the few restaurants that we have in London and Paris. I'm optimistic about that”.

Source: company and own elaboration

With these assumptions, the company should accomplish the 7.000 restaurants by 2033. CEO pointed out they expect an accelerated growth between 8 and 10%. Could be possible, I am going to fix growth at the lower end of the range, 8%. Given the current landscape, I believe is doable.

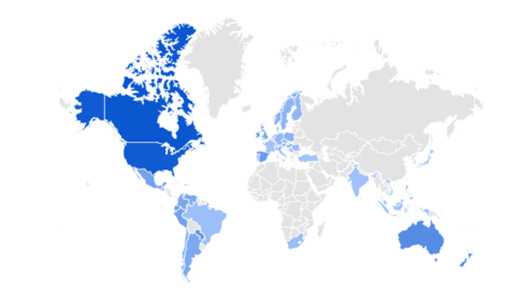

A quick check with Google Trends. The global interest in the word burrito has grown in the last years and there is an interest in Europe and Australia to capture.

Source: Google Trends

3. Margin growth.

We’ve seen the graph before, all-time high. It’s difficult to see it much higher. Automation can help, and a higher share for digital ordering too, but competition is fierce, and a much higher margin in a sustainable way is not a probable scenario in my view.

Source: company and own elaboration

Financials

Balance Sheet

· The first thing to mention is how we can see in the balance sheet the no-franchise business model, with a weight of operating lease assets of 47.7%.

· The balance sheet is lower than the annual revenue. So asset turnover is high, key for the return of the business.

· Inventory turnover ratio of 6,3 per month. A number in between of what is expected from a restaurant, between 4 and 8 times a month. A really good inventory management.

· Working capital in the positive territory is 27% higher as of the end of 2022. Investment increased considerably in 2022, 43% of current assets. That item captures the investments in US Treasury securities.

· Only operating leases account as debt in the balance sheet with a number of $3.73B. No financial debt. Final Net debt/EBITDA ratio of 1,1x as per the second quarter of 2023. All solvency ratios are in a remarkable zone.

· The balance sheet is in really good shape. Healthy and ready to expand.

Income Statement

· In terms of sales, it wouldn’t be wise to extract conclusions given the food poisoning and COVID episodes. However, sales growth is at good levels.

· In terms of costs, there have been important increases. A 2022 versus 2019 (pre-Covid) comparison:

o Food: 34,6% increase

o Labor: 38% increase. Restaurants are all staffed (95%), although they had to increase wages by around 20% recently. Now, they’re seen normalized levels of wage growth, mid-single digits.

o Occupancy: 18,7% increase

o Other operating costs and SG&A: increases of 27,4% and 215

· Sales are almost 100% in USD, therefore foreign currency risk is not material at this date.

· Return on capital of 55,8%. CFROI = CFO/Capital Employed, this last one being: total equity, long and short-term, and capital leases. If I would consider operating leases too, the number would decrease to 21,7%. No doubt they don’t want to franchise.

Cash Flow Statement

· A persistent increase between CFO and Net income due to, chiefly, depreciation and stock-based compensation. For the last element, we are talking an average of about 6% of labor costs. FCF margin is currently around 10%.

· Capex is approximately 6% of sales. Last year Chipotle spent 479,2M in 2022.

Source: company and own elaboration

Valuation

In order to carry out the valuation, I take into account the following assumptions:

· The growth in average restaurant sales is going to be the average annual growth achieved in the last 5 years. Maybe they can grow quicker. I take a more conservative approach.

· About new locations’ growth, they’ve expressed they’d like to see an 8-10% growth here. Let’s leave this year with almost a 7% for later considering the lower range of the management guidance. Reaching more than 7.000 locations for 2033.

· In terms of margin, a little improvement in labor, occupancy, and food, beverages, and packaging. From a fcf margin of 9,8% in 2022 to 11,2% in 2026.

· WACC of 6,5% and a growth of 3%, a little higher than the “standard” of 2% given the tailwind we’ve seen at least in retail sales. Enough to justify 100bp extra.

Source: own elaboration

In terms of valuation, considering free cash flow yield (levered in this case, which considers taking into account the company's financial leverage) it could be said it’s currently well-priced with historical multiples. In this regard, my exit fcf yield for 2026, for instance, would be 2,75%.

Source: tikr terminal

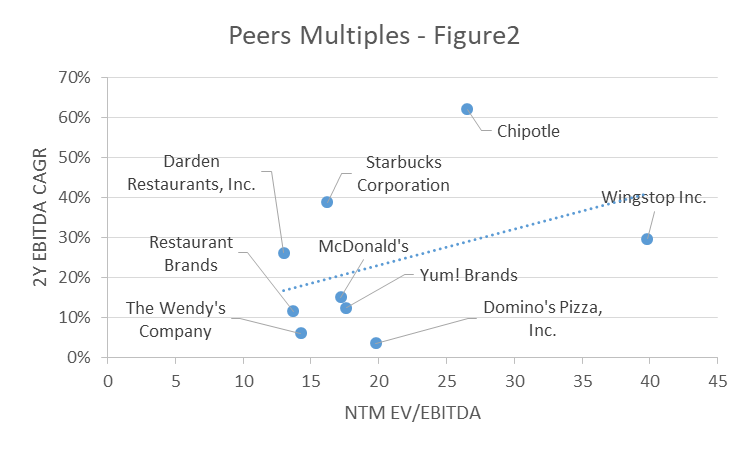

Let’s now take a look at peers:

Source: tikr, koyfin, and own elaboration

It seems like multiples are more sensitive to ebitda growth than margins. Make sense to me. Chipotle is ahead in terms of growth but behind in terms of margin. Margin is dependent on the business model, i.e. Chipotle does not franchise, McDonald’s does.

After seeing all these numbers, the profile of the company, the growth expected, and its value proposition I believe the company is well-positioned for the future ahead. I am not sure about the future expansion internationally. There is not such a strong culture for Mexican cuisine in Europe for instance and for that reason, I believe at some point they will achieve a certain level of maturity. Also, we would be doing well not forgetting about the food poisoning episodes that affected heavily the stock performance. That could happen again, although incentives are well aligned to minimize the chances.

Management and Ownership

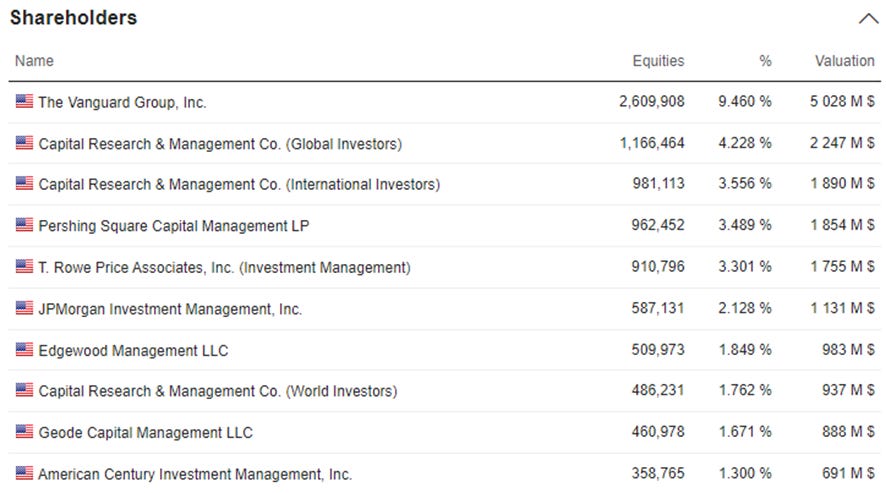

I start with the shareholding, as we can see, the control is mainly in the hands of private investment vehicles. From this list, we can stop a little bit on Pershing Square.

Bill Ackman is at the top of the list. He started buying when everyone else was cutting positions in the company, around 2016. He defends the company has room to grow in comp sales and in the number of locations. Also pointed out something interesting, daypart expansion such as breakfast. A couple more things, Pershing Square helped with the new management transition and defended strongly the digitalization of the company.

About management, Chipotle’s CEO is currently Brian Niccol, 46. Niccol joined Chipotle as CEO in March 2018 and was previously running the show at fast food chain Taco Bell. I appreciate Niccol’s relatively young age. The other important leaders in Chipotle, most of whom have relatively young ages too (a good thing I’d say), include:

Source: company

About compensation and alignment:

The 2022 base salary for the CEO is $1,250,000, which means that the whole package could be of almost $18,000,000.

Source: company

Annual Bonus: tied to company performance factor + individual performance factor modified by ESG performance and food safety. The company performance factors include comparable restaurant sales, restaurant cash flow margin, and site assessment requests.

The Long-term Incentive (LTI) mix for 2022 was 60% PSUs ( performance stock units), tied to a three-year performance period. 20% seven-year stock-only stock appreciation rights (“SOSARs”) that vest in two equal installments on the 2nd and 3rd anniversaries of the grant date, and 20% choice between SOSARs or RSUs that vest in two equal installments on the 2nd and 3rd anniversaries of the grant date. For 2022, all executives elected to receive SOSARs, resulting in LTI value being granted 60% in PSUs and 40% in SOSARs.

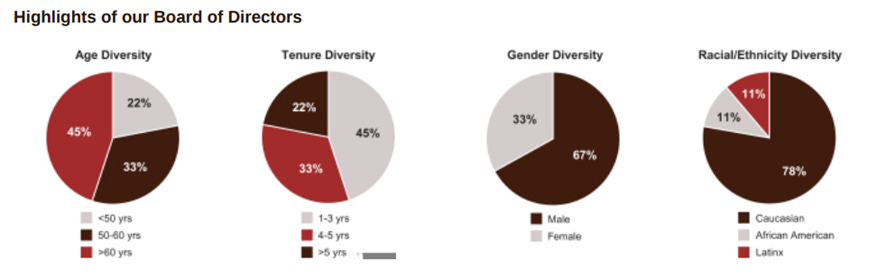

The Board of Directors is composed of 9 members, of which 8 are independent. The CEO is the only executive on the board.

Source: company

I noticed E&Y has been the auditor since 1997, they should consider a change.

ESG

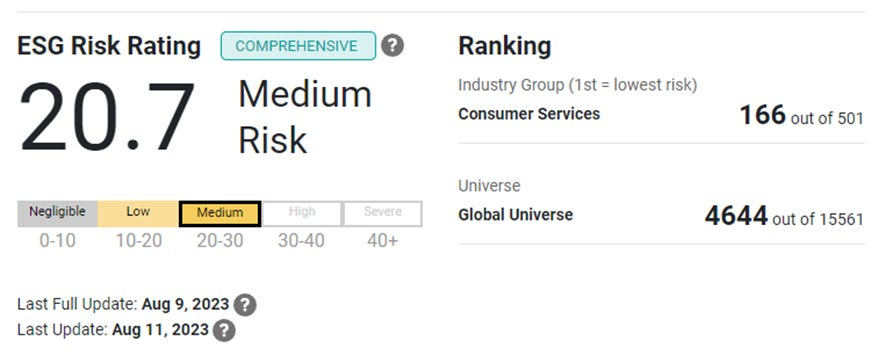

We’ve seen how management has ESG targets, although the ESG scorings (Sustainalytics and MSCI) are not the best. I assume that past episodes of food poisoning and where employees were encouraged to go to work although ill, don’t leave the company in the best position.

In terms of decarbonization targets, they are aligned with the temperature target signed in the Paris Agreement and they expect to reach carbon neutrality for 2030. For instance, Scope 1 & Scope 2 GHG emissions are 13% below 2019 GHG emissions.

I think also it’s a good thing to remember in this section about the Restaurateur program which allows hourly crew members to become managers earning well over $100,000 a year.

The approval from employees is not bad for that kind of business.

Source: glassdoor.com

ESG Rating

SWOT Analysis

Strengths & Opportunities

There’s an important tailwind in restaurant sales, as an industry, with a CAGR of 5.9% in the last 20 years. For the fast-casual market, it’s expected a CAGR of 11.56% between 2022 and 2027.

Brand recognition, being the preferred Tex-Mex chain in the US.

Vertical integrations: secured a well-organized supply chain with 26 independently owned and operated regional distribution centers.

Tex-Mex is the best category selling in the fast-casual niche in the US.

Capacity to pass some cost inflation to customers.

Store-level margin and average restaurant sales are upward trending and at their best.

The payback period is minimum in the industry with an average of almost two years.

I consider Pershing Square a good asset to have on the ownership list.

Growth ahead is undeniable in the three aspects:

Sales per restaurant will most likely continue its trend. The company is constantly engaged with social media, new products, and data that will allow them to empower the most accepted innovations.

Regarding restaurants, they expect 7.000 shortly. International expansion, with higher US penetration, will make it possible. I hope the non-US restaurants have the same profitability profile.

And, in terms of margin, it is going up and the investments in efficiency are not going to stop soon. A higher use of digital channels, AI, and a more intensive use of robots will allow the company to keep improving its margin.

The food served is mostly a really good thing, although a risk too, I believe it’s greatly appealing to have a $10 average dish, which can be truly healthy, in which the customer can control the calories, the fat, the protein, and the carbohydrates. That could prove to be a better selling point in Europe than in the US.

The company invests heavily in the workforce. That’s more a requirement, in my opinion, than a choice given that to run the business they need a lower turnover than the industry. Nevertheless, a win-win situation.

Loyalty programs exploded in recent years even been a late player in that field. A good practice that we’ve seen is how well it works in companies like Starbucks or Amazon.

The interest in the food that Chipotle is offering is upward trending and in second place, after Italian/pizza choice.

Chipotle is one of the biggest Mexican food restaurants, after Taco Bell. With the investments we are seeing in tech, data should be a great ally for the years ahead.

Balance Sheet is healthy, with room to expand if needed.

Chipotle does not have a dividend commitment, which allows them to keep investing in growth.

Weaknesses & Threats

It’s great to have fresh food in the meal, but its management is riskier than frozen food. The last big episode should be using a good reminder of what could happen again and what a great risk this could be for the shareholder.

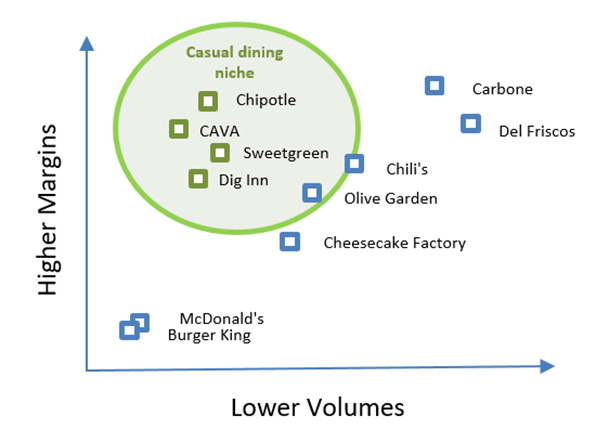

The formula has proven to work well and with low barriers to entry, we can see new competitors in the space of fast-casual, such as CAVA.

I consider aggregators a threat, although at first, they may expand the TAM, they will keep part of the data and keep a part of the margin.

Finding local farmers with capacity and international reach, or local farmers outside the US, could be a difficult task.

Consumption in restaurants is decreasing in the short term.

Final Remarks

Chipotle has been a good surprise. They have, apparently, a simple business model but highly profitable, easy to understand, and without great disruptions in the industry, an affirmation that could be interpreted as stability. The company has had food issues in the past, which ended up in a new management team and, the hiring of Taco Bell’s CEO at the time, and since then, time and new procedures have contributed to a stellar performance, from a business and stock performance standpoint.

The foundations for growth are well settled and management and market participants are optimistic about the future of the company. I couldn’t agree more. However, like most good things in life, it doesn’t come cheap. Under my estimation, the 2023 expected free cash flow yield is 1.9%. Clearly expensive, but really close to the historical average. Based on current estimations, that multiple is 2,26%.

I am sure the market is expecting a big decrease in rates soon, meanwhile, the US Treasury is reaching new highs in yields and I’ve at some point feared to be higher for longer, Chipotle is poised to receive an important hit in terms of valuation. The current 34x for NTM PE is way higher than the S&P 500’s forward PE of 19x. Nevertheless, it seems that a technical pullback could be a good entry point in the short term. A company to hold if the thesis stays.